[d3-source canvas=”wpd3-13124-0″]

Microfinance was speculated to be the magic bullet, end-all cure for poverty. In 2006, Professor Muhammad Yunus and the Grameen Bank won the Nobel Peace Prize for spearheading this innovative movement, lending small amounts of capital to impoverished women in India in order to lift them out of poverty. The microfinance industry declared its goal of “financial inclusion,” which they believed consisted of access to credit, insurance and other financial products. The gloss has started to come off in recent years, as the long-standing claims of poverty alleviation and female empowerment came to be challenged. The validity of those claims, as well as the effectuality of microfinance, now stands unclear and thereby negligible. However, there is simply too much at stake for the public good to let the questions linger unresolved.

Yunus defined “social business” as an enterprise for the public good, which he deems “the new kind of capitalism.” He founded Grameen Bank, pioneering the practice of microfinance, which provides financial services to low-income individuals, of whom over 95% are low-income women. Importantly, Yunus managed to demonstrate that the poor are not unreliable borrowers, and can thereby benefit from learning how to use credit.

The mission has faced some obstacles in its implementation. The Grameen bank has its ardent supporters and fierce opponents, which has clouded its reputation. This is largely due to controversy surrounding Yunus, who is seen as a polarizing figure in Bangladesh, where the bank is centered. Personal attacks denouncing Professor Yunus can be traced to his poor relationship with the government.

Yunus made a brief stint into politics in 2006 when he attempted to form his own political party. The announcement was ill-timed, as it coincided with a military crackdown on dozens of government officials who were charged with corruption. Prime Minister Sheikh Hasina herself was put under arrest a few months later. Hasina may have seen Professor Yunus’s move as a deliberate effort to challenge her political standing. Thus began a not-so-subtle campaign to slander Yunus and the Grameen Bank. Reports promptly came out about desperate borrowers being charged exorbitant interest rates. Hasina herself voiced that the bank was “sucking blood from the poor.” The Yunus Center website issued a “questions by critics… and the facts” page to challenge reports that were circulating about Mohammed Yunus’ questionable character and practices with regard to the Grameen Bank. They list about thirty questions defending the integrity of Yunus and the bank, denying accusations that range from evading taxes, embezzlement, deceiving the public, to being a “traitor to his country.”

In defense of the claim that Yunus hasn’t been leveraging his international influence for the benefit of his country, the site claims that, “Professor Yunus would be very happy to play a role in solving problems of Bangladesh. But someone has to make use of him.” The site points out how the government fails to show Yunus support at international events, which reflect poorly on both him and the government. According to this account, “everyone wants to know why the Bangladeshi Ambassador is absent.” Yunus’ defense of his ideas and the Grameen bank has largely amounted to placing the blame on the unwarranted obstruction from the government.

The government of Bangladesh successfully organized a campaign to remove Yunus from his position as leader of the bank. A court case was brought against Yunus and it was ruled that at 70 years of age, Yunus was required by law to step down as managing director when he turned 60, and that the belated enforcement of that requirement was legally valid. The efforts to push him out seem to Yunus and his many ardent supporters around the world, including the American government, as a politically-motivated use of a technicality.

That said, the criticism of Yunus is not completely unfounded. BBC Bengali editor Sabir Mustafa described Yunus’ negative qualities that in part demonstrate why he is such a polarizing figure. Mustafa noted that after a speech Yunus made at a UN conference, “He showed little willingness to engage with the Bangladeshi media, even when approached. People often feel he is not prepared to face, let along answer, critical questions about the way Grameen Bank operates.”

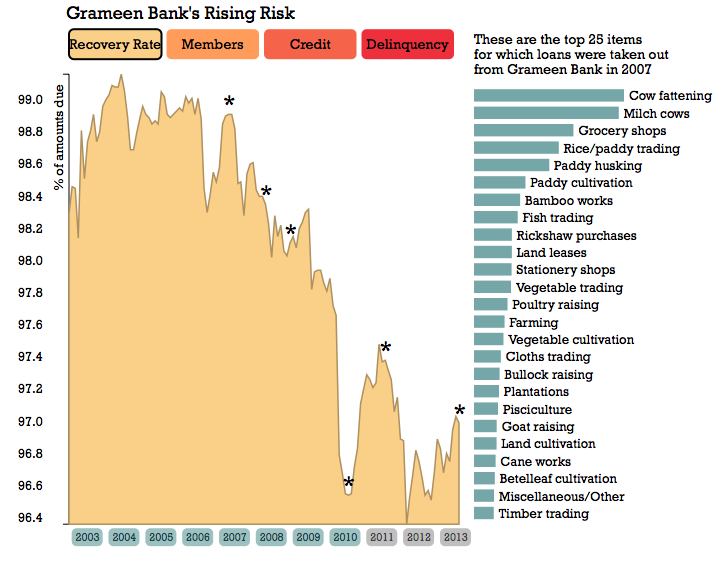

The discourse around Yunus certainly contributed to the mixed reputation of Grameen Bank. However, the question of whether microfinance is an effective and viable business model must obviously be considered on its own terms. Critics of microfinance often argue that these institutions exacerbate the cycle of poverty. At times, the borrower doesn’t have enough time to establish an income-earning business to cover the initial repayment, which can led to more loans from different sources. Dr Qazi Kholikuzzaman Ahmad, chairman of PKSF, a body that monitors microfinance, describes this process as a “death trap” for the borrowers. He explains how 60% of borrowers take loans from several sources and that “There is no understanding that it might take 10 or 20 years to repay their loan.” However, Grameen’s supporters are numerous and these claims have been convincingly debunked. By and large, it still seems that there is no resounding consensus on the success of Yunus’ efforts or microfinance initiatives at large. No study has been comprehensive enough to examine the benefits and costs of this program. This is also complicated by the observations of an independent economist, Kathleen Odell, who determined the “overall effect on the incomes and poverty rates of microfinance clients is less clear, as are the effects of microfinance on measures of social well-being, such as education, health, and women’s empowerment.” This conclusion seems confusing, but is likely because microfinance is not one simple practice. It may involve loans, savings, training, services and combinations of all of these things. Importantly, these transactions take place in distinctive circumstances, and their effects unfold overtime, so long-term impact is difficult to observe in a study.

Whether it was the mixed reporting of Grameen Bank’s success or Yunus’ controversial character that primarily dampened excitement around microfinance, both have certainly contributed. The complete narrative around the Grameen Bank is actually pertinent and revelatory about the way social business works in real life; government support of socially responsible initiatives — financially or otherwise — can be a critical factor in its success.

How ridiculous it is to see Carly quoting BBC Bengali editor’s grievance against Dr Yunus for not giving him an interview after his UN speech. How not interacting with a Bangladeshi journalist could make a man ‘polarizing figure’?

This is awesome. Great job Myles, and fascinating article Carly.